2. How do these insights affect the world of sovereign debt?

3. How does it affect the U.S.?

1. What new insights has the IMF gained from the #GreekCrisis?

The IMF's recent report on the Greek Crisis identified several new insights, three of which are quickly changing the policy dialog on sovereign debt.

FIRST: Democracies find it very difficult to sustain a primary surplus (live within their means).

Countries calculate "living within their means" differently than households. Households generally add up all their income, then subtract all of their expenses and their debt payments, and if there is any money left over, they are "living within their means". Countries on the other hand add up all their income, then subtract only their expenses (without including any debt payments of interest OR principal) and if they have anything left over it is called a "primary surplus" and is considered to mean they are "living within their means". Of course their creditors want them to have some primary surplus so they can make payments on their debts, but many countries (including the United States) simply borrow more money to make their debt payments. The first two rounds of bailouts for Greece were intended to help them get to a point where they were living within their means (running a primary surplus). And they did it!! But once they started running a primary surplus the people elected a new government that promised to relieve the pain of austerity imposed by living within their means. The IMF has stated that this change in policy has resulted in making the Greek debt load "unsustainable". The new insight for the IMF seems to be that in democracies where living within their means is particularly painful, the people will elect governments that will implement pain-reducing fiscal policies that often increase the debt load. I'll call this the "pain relief democracy" insight.

SECOND: Relatively small policy changes can produce sudden large increases in debt burden

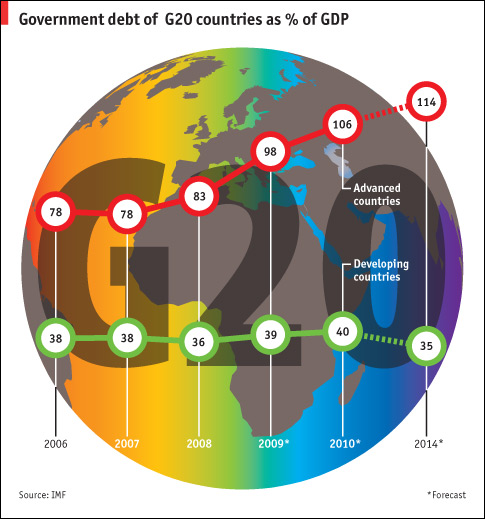

Until just recently Greece was running a primary surplus and looked like it would be able to keep its debt load near the IMF target of 110% of GDP. Within just a few months of relatively small policy changes, Greece's debt load has skyrocketed to 170% of GDP and is expected to rise about 200% of GDP even assuming they DO get a substantial new bailout. I'll call this the ""sudden debt growth" insight. The IMF was clearly surprised by how quickly the debt situation deteriorated in Greece over the past few months.

THIRD: The best way to restore Greece to sustainable growth in the EU is through substantial debt forgiveness.

Historically when a country couldn't pay their debts, the normal response of creditors was to extend the repayment period and/or reduce the interest rate. This is exactly what was done with Greece in the last two rounds of "debt restructuring" bailouts. The IMF is now saying that this approach is not their preferred approach with Greece. They insist that what needs to be done is for a large portion of the Greek debt to be forgiven outright. This is precisely what European leaders are strenuously resisting and what Greek leaders have been insisting on. The IMF has now moved firmly into the debt forgiveness camp. This is what I call the "debt forgiveness" insight.

2. How do these insights affect the world of sovereign debt?

The combined impact of the these new "insights" is a growing possibility that much of the sovereign debt in the world today may be "inflated" in value. In other words, there may be more risk in sovereign debt than is currently reflected in the prices for this debt.

"Pain Relief Democracy" Insight:

Much of the world's sovereign debt is held by democracies. While most of these democracies have debt levels below 140% of GDP (a level considered sustainable), if their debt levels continue to climb (as they have for many years) until it becomes "painful" to service their debt, these democracies will be inclined to elect governments that will promise to relieve the pain even if the creditors don't get paid in full or on time.

"Sudden Debt Growth" Insight:

Debt ratings and prices of sovereign debt are based on carefully considered expectations about the ability and willingness of debtors to pay their debts on time. One of the biggest surprises coming from the Greek crisis over the past few weeks is the realization of how quickly a country's debt levels can go from "sustainable" to "unsustainable". Everyone involved - European Bankers, European Heads of State, the IMF, and even the Greeks themselves - seem to have been completely surprised by how quickly Greece's debt burden went from 140% of GDP to a projection of over 200% of GDP. This possibility of "sudden debt growth" has not been priced into much of the sovereign debt market.

"Debt Forgiveness" Insight:

This is a big one. Debt forgiveness for banks represents the difference between "return ON investment", and "return OF investment". When there is a heightened prospect that a lender won't get their investment back at all, let alone with interest, the risk profile (meaning price) of the debt changes dramatically. For example, in contrast to low-risk sovereign debt loans to developed countries, Venture Capitalists play in a very high risk market. They lose some or all of their investment on most of their investments, but the returns are so large on the few that do succeed that their overall return can still be very high. However pricing of sovereign debt in the developed world is perceived to be low risk and assumes a very low risk that a developed country like Greece would actually default on significant portions of their debt. In the past two weeks, the IMF has insisted that this very possibility must be introduced into the sovereign debt discussions for developed countries. The increased possibility of significant debt forgiveness has not been priced into the sovereign debt market for developed countries.

3. How does it affect the U.S.?

The net effect in the short term of these new insights for the U.S. is probably very favorable. Once the full risk of these insights is properly priced into the sovereign debt markets, the interest rate for sovereign U.S. debt is likely to go DOWN while the risk premium for other nations' debt will likely go up (this has already begun to occur in Europe with German debt versus riskier sovereign debt from other countries in the EU). However if the markets perceive all sovereign debt to be overpriced based on a new sense of the risks, we could discover the existence of a sovereign debt bubble by the effects of its bursting - just like we did when the housing bubble burst. Fortunately this is not a high-probability event.

No comments:

Post a Comment